Scenario 9

|

Scenario 9 |

|

|

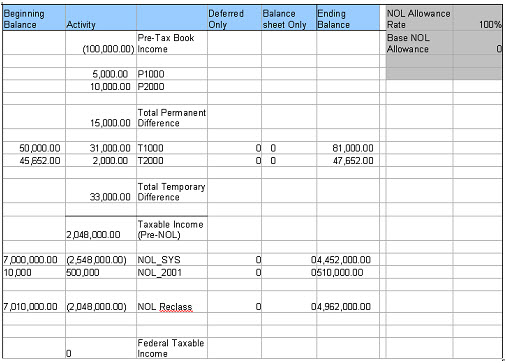

When the NOL Allowance Rate is set to 100%, the Base NOL Allowance to 0, and there is another NOL Temporary Difference with Activity (500,000), the NOL Reclass is the sum of 100% of the Federal Taxable Income (2,048,000.00) and the NOL Temporary Difference (500,000). [(2,048,000.00) <Federal Taxable Income> + (500,000)< NOL TD>] – 500,000 <NOL TD> = - 2,048,000.00 <NOL Reclass>

If the NOL Reclass is added to the Federal Taxable Income (Pre-NOL), the Federal Taxable Income (Post-NOL) is 0. 2,048,000 <TI Pre-NOL> + -2,048,000 <NOL reclass> = 0 <TI Post-NOL>

NOL Ending Balance (Beginning Bal + Deferred Only + Balance Sheet Only) + (NOL Reclass) = NOL End Bal (7,010,000 <BBal> + 0<DO> + 0 <Bal O>) + (-2,048,000 <NOL Reclass>) = 4,962,000 <EB>

Note: To access the report, select the Reporting area, Dataset, and Report Level. Then, in the navigator select Tax Provision and click Run. View Detail. On the report, select the View Detail hyperlink.

|