AFTER TAX TEMP diffs

|

AFTER TAX TEMP diffs |

|

|

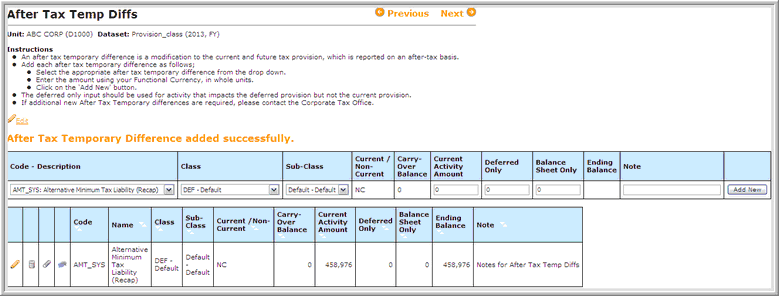

In the After Tax Temporary Diffs page, users can enter after tax adjustments that are temporary in nature. An example of an After Tax Temporary Difference is a tax credit with a carry-forward amount.

Enter a separate line item for each after tax temporary difference:

After an after tax temporary difference item is created, users can edit or delete it by clicking the appropriate icon.

Global Access users can enter information in the current activity, deferred only, and balance sheet only fields using the income statement approach. Users can input an ending balance amount and have the program calculate the current activity using the balance sheet approach. Administrators can activate the balance sheet approach through a parameter. However, even with this parameter, Global Access users still have the option to take either approach for each line item.

Notes:

|