PERMANENT DIFFS (GAAP/STAT)

|

PERMANENT DIFFS (GAAP/STAT) |

|

|

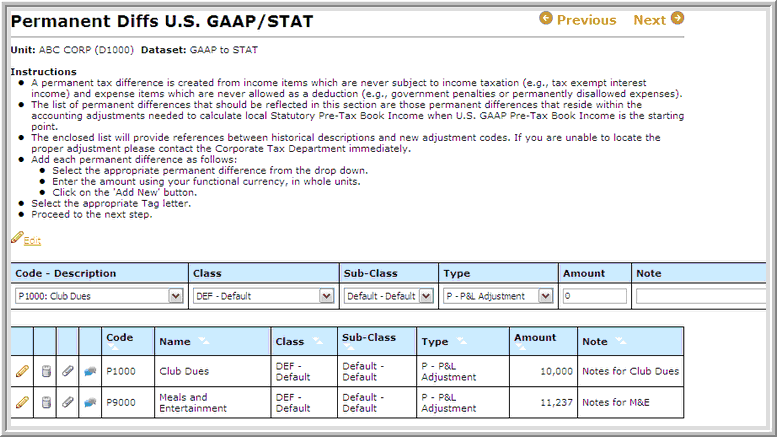

In the Permanent Diffs GAAP/STAT page, users can enter permanent differences that are permanent in nature (the difference between book income computed for US GAAP and Statutory income in the country). These differences will not reverse in the future. Some examples of permanent differences include; permanent disallowed expenses, certain types of goodwill amortization, and tax-exempt interest. Administrators must select this page in Manage User Permissions for users to view the page. Permissions.

Enter a separate line item for each permanent difference:

After a permanent difference is created, users can edit or delete it by clicking the appropriate icon. 1. Click the pencil icon to edit the permanent difference. 2. Select Save Changes after updating the permanent difference.

Notes:

|